Understanding the insurance landscape for hatchbacks in the United Arab Emirates requires a granular look at vehicle specifications and physical condition. Insurance premiums are not arbitrary figures; they are calculated based on the probability of a claim and the cost of repair for a specific vehicle type. For hatchback owners, where compact size and agility often lead to higher accident frequencies in urban environments, the vehicle's condition plays a decisive role in determining premium rates. A comprehensive understanding of how vehicle type interacts with inspection findings can save significant costs over the lifespan of the car.

The Anatomy of a Hatchback Premium

Insurance providers categorize vehicles based on their market value, repair costs, and theft susceptibility. Hatchbacks generally fall into the subcompact or economy segments, meaning their replacement values are lower than sedans or SUVs. This lower valuation directly influences the premium, as the insurer faces a lower liability payout in the event of a total loss. However, this does not mean these vehicles are cheap to insure against damage. High-performance hatchbacks, such as hot hatches, often command higher premiums due to the increased risk associated with aggressive driving and the specialized parts required for repairs.

The age of the vehicle also dictates the premium structure. Newer hatchbacks benefit from lower depreciation, meaning their current market value is higher, which can increase the premium. Conversely, older models often see reduced premiums due to lower values, provided they retain mechanical integrity. Insurers assess the risk profile by looking at the vehicle's engineering and the likelihood of mechanical failure, which brings us to the critical intersection of vehicle condition and insurance pricing.

The Critical Role of Vehicle Condition

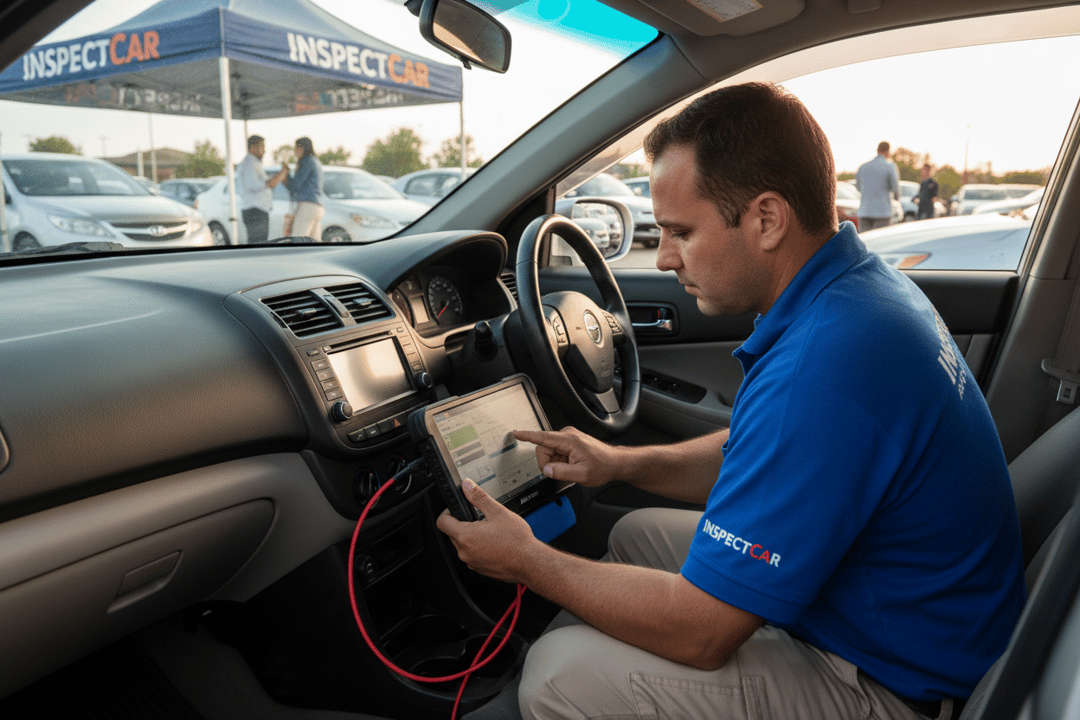

A vehicle's physical and mechanical condition is the single most influential factor in determining insurance premiums. Insurers view a well-maintained car as a lower risk profile compared to one with hidden defects. If a vehicle requires significant repairs or has a history of poor maintenance, the insurer will adjust the premium to account for the higher probability of a claim. This is where a professional inspection becomes essential for owners looking to understand or challenge their insurance rates.

Pre-inspection reports provide a transparent view of the vehicle's health before an insurer evaluates it. A documented history of maintenance and a clean inspection report can serve as leverage when negotiating premiums. It demonstrates to the insurer that the vehicle is roadworthy and less likely to suffer significant failure. Ignoring minor issues can lead to snowballing problems that eventually result in a total loss or a claim that spikes the insurance cost for subsequent years.

Key Inspection Categories That Impact Rates

Inspection findings are scrutinized across several key categories to determine a vehicle's insurability and associated risk. These categories cover everything from the structural integrity of the vehicle to the safety of its braking systems. Understanding these checkpoints helps owners identify potential rate-increasing factors before they submit a claim.

- Body and Paint: Inspectors analyze panels to determine if a vehicle has been repainted, which can hide previous accident damage. Identifying original paint versus repainted areas is crucial for assessing whether a car was involved in a collision that compromised its safety features.

- Frame Integrity: Structural components, including rails, pillars, and the floor pan, are inspected for bending or corrosion. Frame damage is a major red flag for insurers, as it affects the vehicle's ability to protect occupants in a collision and often leads to higher repair costs.

- Engine and Transmission: The engine is the heart of the vehicle. Inspectors listen for unusual sounds, check for leaks, and review smoke color during the test drive. Engine failure is a primary cause of insurance claims, and a failing engine significantly raises the risk profile.

- Braking System: The percentage of brake pad wear is rated to assess remaining stopping power. Worn brakes increase the likelihood of accidents, making this a key factor in premium calculations.

- Suspension and Tires: Shock absorbers, struts, and tire manufacturing dates are checked. Proper suspension ensures vehicle stability, while tires with low tread depth or incorrect manufacturing dates are immediate safety hazards.

Technical Diagnostics and Hidden Risks

Modern vehicles rely on complex computer systems to manage engine performance, safety features, and emissions. An OBD scan is an indispensable tool for identifying issues that are not visible during a visual inspection. Engine, transmission, ABS, and airbag codes can point to latent failures that may not manifest immediately but pose a significant risk on the road.

Fluids play a vital role in vehicle longevity. The level and condition of engine oil, coolant, and brake fluid are checked to ensure they are within manufacturer specifications. Low or contaminated fluids can lead to overheating or brake failure, both of which are catastrophic events that result in high-value claims. For hatchback owners, where space is premium and mechanical issues can be more difficult to service than in larger vehicles, maintaining these systems is financially prudent.

| Inspection Package | Service Price | Key Focus Areas |

|---|---|---|

| Computer Diagnostic | AED 99 | Engine/Transmission, ABS, Airbag Codes |

| Body & Computer | AED 250 | Panel-by-panel paint analysis, OBD scan, structural checks |

| Comprehensive Inspection | AED 299 | 410+ checkpoints including frame, fluids, brakes, road test |

Structural Integrity and Accident History

When a hatchback is involved in an accident, the cost of repairs can exceed its market value, leading to a total loss. Insurers use inspection data to assess whether a vehicle has a clean chassis or if it has undergone structural repairs. A vehicle with repaired pillars or a damaged floor pan may be classified as having increased structural deformation, which compromises its safety ratings.

Paint analysis is a sophisticated method used to detect accident history. Inspectors look for color inconsistencies, different thicknesses in paint layers, or signs of heat distortion. These markers indicate whether a panel has been replaced or repaired, which directly impacts the vehicle's value and insurability. A vehicle with a documented history of structural repairs is inherently riskier to insure than one with a clean chassis, often resulting in higher premiums or the denial of coverage for specific parts.

Preventative Measures for Owners

Preventative maintenance is the most effective way to keep insurance premiums low. Regular servicing ensures that the vehicle operates within manufacturer tolerances, reducing the likelihood of mechanical failure. Owners should prioritize safety systems, ensuring that brakes and tires are replaced before they reach critical wear levels.

Utilizing professional inspection services provides a baseline for vehicle health. An inspection uncovers hidden issues that could later become expensive claims. For buyers, a pre-purchase inspection is a necessity to ensure they are not purchasing a vehicle with a history of accidents or mechanical issues. For sellers, a clean inspection report can justify a higher selling price and reassure potential buyers. By addressing these factors proactively, owners protect their investment and minimize the financial burden of insurance premiums.

AutoFay inspects 410+ checkpoints with HD photos and PDF report. Book at autofay.ae or call +971542584458

0 Comments

No comments yet. Be the first to share your thoughts!