When you’re eyeing a used Ford Territory 2025 or a second‑hand Honda HR‑V 2022, the financing part often feels as complex as the engine bay. Knowing how banks and dealers structure loans helps you avoid costly surprises later. Below is a mechanic’s take on the numbers, the paperwork, and why a pre‑ inspection is non‑negotiable.

Understanding the Two Main Financing Paths

Bank loans come directly from a financial institution and usually require you to secure the vehicle as collateral. The bank will assess your credit score, income proof, and the car’s market before granting a line of credit.

Dealer finance is arranged by the showroom’s own finance department, often in partnership with a bank or a captive finance company. The dealer may bundle the loan with optional add‑ons such as extended warranties or service packages.

Bank Loans: How They Work in the UAE

UAE banks typically loan‑to‑ ratios of up to 80 % for a used SUV, meaning you need to fund the remaining 20 % yourself. The loan term can stretch from 12 to 60 months, with monthly payments calculated on a reducing‑balance method.

Interest rates on bank loans are usually linked to the Emirates NBD base rate plus a spread that reflects your risk profile. A higher credit score can shave off a full percentage point, translating into thousands of dirhams saved over the life of the loan.

Dealer Finance: What to Expect

Dealers often advertise “0 % financing” for a limited period, but the true hides in higher vehicle prices or mandatory insurance policies. The loan term may be shorter, pushing you to clear the balance before the promotional period ends.

Because the dealer controls the paperwork, they can add processing fees that are not disclosed until the final contract. These fees can erode the apparent and increase the effective interest rate.

Interest Rates, Fees, and Hidden Costs

Below is a side‑by‑side of typical bank dealer financing structures for a used Ford Territory 2023.

| Financing Source | Typical Interest Rate | Common Fees |

|---|---|---|

| Bank Loan | 3.5 % – 5.5 % | Processing fee (≈ a notable sum), early‑repayment penalty |

| Dealer Finance | Effective 6 % – 9 % | Administrative surcharge, bundled insurance premium |

Even a half‑percent difference compounds over a five‑year term, turning a modest significant repair costs loan into a notable sum‑plus in interest.

Why Banks Insist on a Pre‑ Inspection

Before a bank releases funds, it wants assurance that the asset won’t lose abruptly. A hidden rusted frame on a Honda HR‑V 2022, for example, could trigger a sudden drop in resale.

Banks also protect themselves from liability if a vehicle’s engine fails shortly after. Burnt transmission fluid, which indicates overheating, often leads to gearbox failure within months—a risk banks cannot afford.

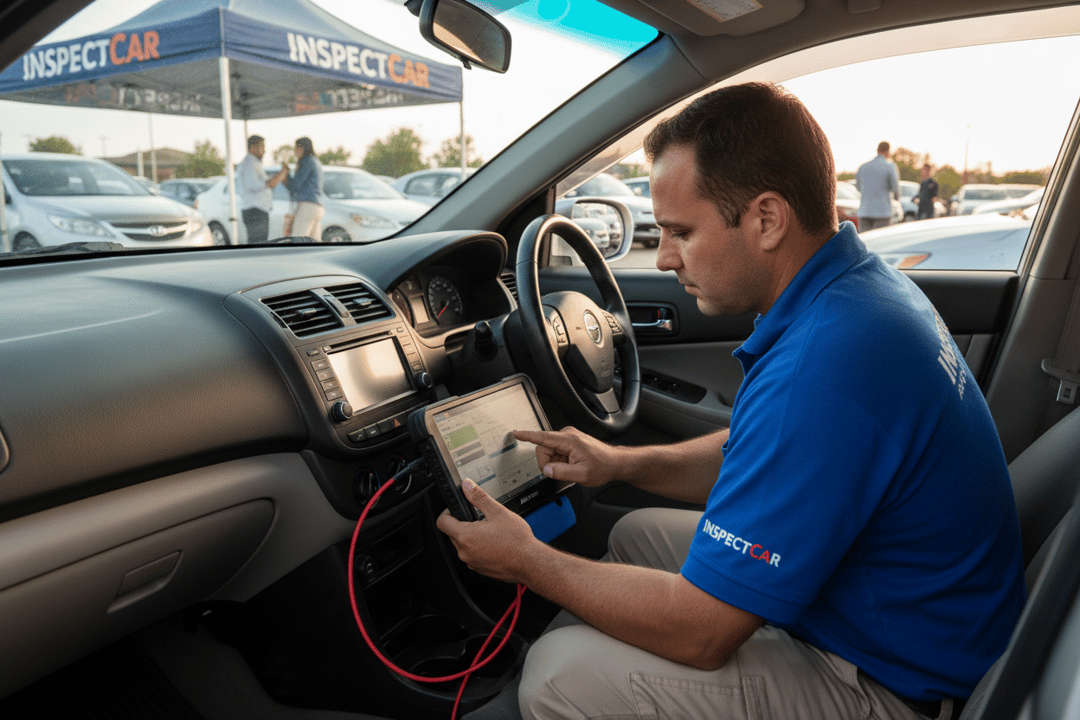

Using AutoFay to Safeguard Your

AutoFay runs 410+ checkpoints across 25 categories, giving you a data‑driven picture of the car’s condition before any loan is signed. Their on-location inspection reaches all seven Emirates, so you don’t need to drive the car to a workshop.

Three inspection packages are available:

- Computer Diagnostic – AED 99

- Body & Computer – AED 250

- Comprehensive – AED 299

The Comprehensive package covers body/paint analysis, frame integrity, engine sound and mounts, OBD codes, brake pad wear, suspension health, tire age, fluid condition, and a road test. Each point is documented with high‑definition photos and a PDF report.

For a Ford Territory 2025, the inspection will reveal if any panels have been repainted, whether the chassis rails show fatigue, and if the engine’s smoke color hints at oil burning. Catching these issues early prevents future repair bills and keeps the loan-to- ratio honest.

When you receive the AutoFay report, you can negotiate the with the seller or ask the dealer to fix the highlighted problems. This negotiation directly lowers the amount you need to borrow, which in turn reduces the interest you’ll pay.

Practical Steps Before Signing the Loan

- Request a full AutoFay Comprehensive inspection and keep the PDF for the bank’s file.

- Compare the bank’s quoted interest rate with the dealer’s effective rate after fees.

- Calculate the total of ownership, including any required repairs uncovered by the inspection.

Following these steps ensures the financing you choose aligns with the car’s actual condition, not just the seller’s sales pitch.

AutoFay inspects 410+ checkpoints with HD photos and PDF report. Book at autofay.ae or call +971542584458

0 Comments

No comments yet. Be the first to share your thoughts!